Personal Loan vs Credit Card: Which Saves More Money in 2026?

When you need extra money, two common options are a personal loan and a credit card. Both can help cover expenses, but they work differently and can have very different costs over time.

Choosing the right one depends on how much you need to borrow, how quickly you can repay it, and the interest rate you’re offered. Understanding these differences can help you avoid unnecessary debt and save money.

What Is a Personal Loan?

A personal loan is a fixed amount of money borrowed from a bank, credit union, or online lender. You receive the money upfront and repay it in equal monthly installments over a set period.

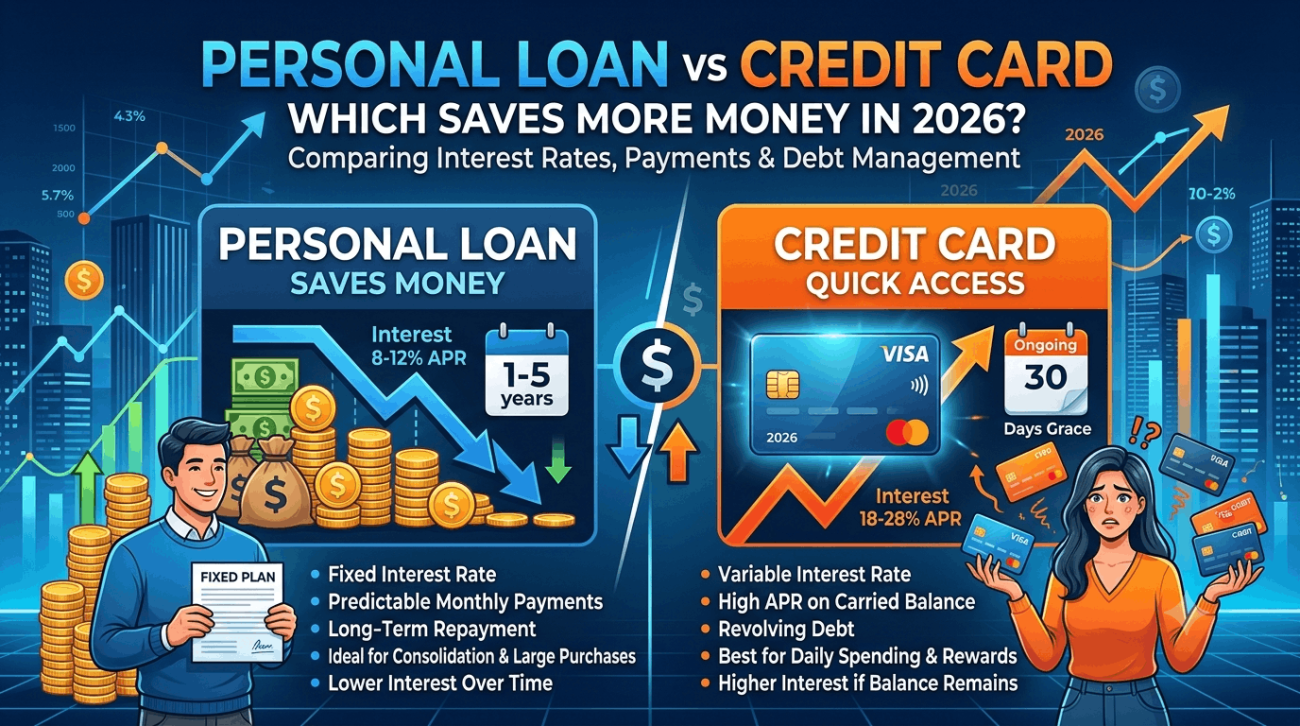

Advantages

- Fixed monthly payments

- Predictable repayment schedule

- Often lower interest rates than credit cards

- Suitable for large expenses

- Can be used for debt consolidation

Disadvantages

- May require a good credit score

- Some lenders charge origination fees

- Missing payments can affect your credit score

What Is a Credit Card?

A credit card gives you access to a revolving credit limit. You can borrow repeatedly up to the approved limit as long as you make the required payments.

Advantages

- Convenient for everyday purchases

- Interest-free period if the balance is paid in full

- Reward points and cashback

- Useful for emergencies

Disadvantages

- High interest rates if you carry a balance

- Easy to overspend

- Minimum payments can keep you in debt for years

Personal Loan vs Credit Card: Key Differences

| Feature | Personal Loan | Credit Card |

|---|---|---|

| Interest | Usually fixed | Usually variable |

| Repayment | Fixed monthly installments | Flexible minimum payments |

| Best For | Large planned expenses | Everyday spending and short-term borrowing |

| Loan Amount | Higher | Limited by credit limit |

| Debt Duration | Fixed term | Can continue indefinitely if only minimum payments are made |

When Should You Choose a Personal Loan?

A personal loan may be the better option if you:

- Need a large amount of money

- Want predictable monthly payments

- Plan to consolidate high-interest debt

- Need funds for home improvements, education, or medical expenses

When Should You Use a Credit Card?

A credit card is often suitable if you:

- Need short-term financing

- Can pay the balance in full every month

- Want cashback or travel rewards

- Need flexibility for everyday purchases

Factors That Affect Borrowing Costs

Several factors determine how much you’ll ultimately pay:

Credit Score

Higher credit scores usually qualify for lower interest rates.

Loan Amount

Borrowing more generally increases the total interest paid.

Repayment Period

Longer repayment terms reduce monthly payments but often increase total interest.

Interest Rate

Even a small difference in interest rates can significantly affect the total repayment amount.

Tips to Save Money

- Compare offers from multiple lenders.

- Borrow only what you actually need.

- Pay more than the minimum credit card payment.

- Avoid late payment fees.

- Review your credit report regularly.

- Build and maintain a strong credit history.

Frequently Asked Questions

Is a personal loan cheaper than a credit card?

In many cases, yes. Personal loans often have lower interest rates than credit cards, especially for borrowers with good credit.

Can I use a personal loan to pay off credit card debt?

Yes. Many people use personal loans for debt consolidation because they may offer lower interest rates and fixed repayment schedules.

Which option helps build credit?

Both personal loans and credit cards can help build your credit history when payments are made on time.

Which is better for emergencies?

Credit cards provide immediate access to funds, while personal loans may take longer to process but can be less expensive for larger amounts.

Final Thoughts

There is no one-size-fits-all answer. A personal loan is generally better for large, planned expenses and structured repayment, while a credit card is ideal for everyday purchases and short-term borrowing when you can pay the balance in full.

Before borrowing, compare interest rates, fees, repayment terms, and your own financial situation. Making an informed decision can help you reduce borrowing costs and maintain healthy financial habits over time.